How to Create a Budget

It’s the new year which means new goals and a new budget! I love taking the time to reflect on previous goals and see how well I did in the past year. It’s easy to feel overwhelmed with personal finances, however, I find when you’re organized, you are more likely to reach your goals and have a better mindset towards money.

I’ve always had the mindset of “You fail to plan, you plan to fail”. I think it’s super important to evaluate what you have, how much you earn, and where you want to go. I find that a lot of people tend to fear checking their bank accounts and some might feel reluctant to be honest about their spending habits.

I am by no means a financial expert, but I am someone that has worked hard to achieve my own financial goals and has learned a lot along the way. Without further ado, here are tips that I have implemented in order to create a realistic budget.

As always, please take my advice with a grain of salt and always consult with a financial professional.

Tip #1: Know Your Spending Habits

What kind of consumer are you? Are you an impulse buyer? What do you usually spend your money on?

Where you spend your money is often what you prioritize. In this step, make sure to be honest with yourself. Check your bank transactions, your Venmo transactions, your credit card statements etc., to better understand where your money is going every month. This can be a jarring experience, however, it’s imperative to know where you’re starting in order to make better habits going forward.

*Note: It’s always important to check your accounts regularly to make sure there aren't any fraudulent purchases or transactions being made. The longer you wait to check and the later you find out, the more money you could potentially lose.

Tip #2: Financial Goal-Setting

After evaluating your expenditures, it’s now time to create financial goals for yourself. What do you want to achieve within the next year, the next five years, in the general future? Are you saving up for a big purchase? Are you wanting to save for retirement? Or simply, do you want to create financial stability for yourself? What does that look like to you?

This is where your budgeting plan comes to life. Having a goal in mind is helpful for you to know the “why”. Why are you budgeting? “Well it’s because I’m trying to save $15,000 this year to go towards retirement”, as a simple example. Getting granular with your goals is important for you to visualize what that looks like and how you can break it down into smaller steps to get there.

Tip #3: Create your monthly budget

This is where you can make your budget completely personal to you. Set a time increment that works with your pay schedule. Whether you get paid biweekly or bimonthly, it makes it easier to set up a budget that aligns with your pay schedule. If you get paid biweekly, I suggest setting a 4 week budget. If you get paid bimonthly, maybe a monthly budget works better for you.

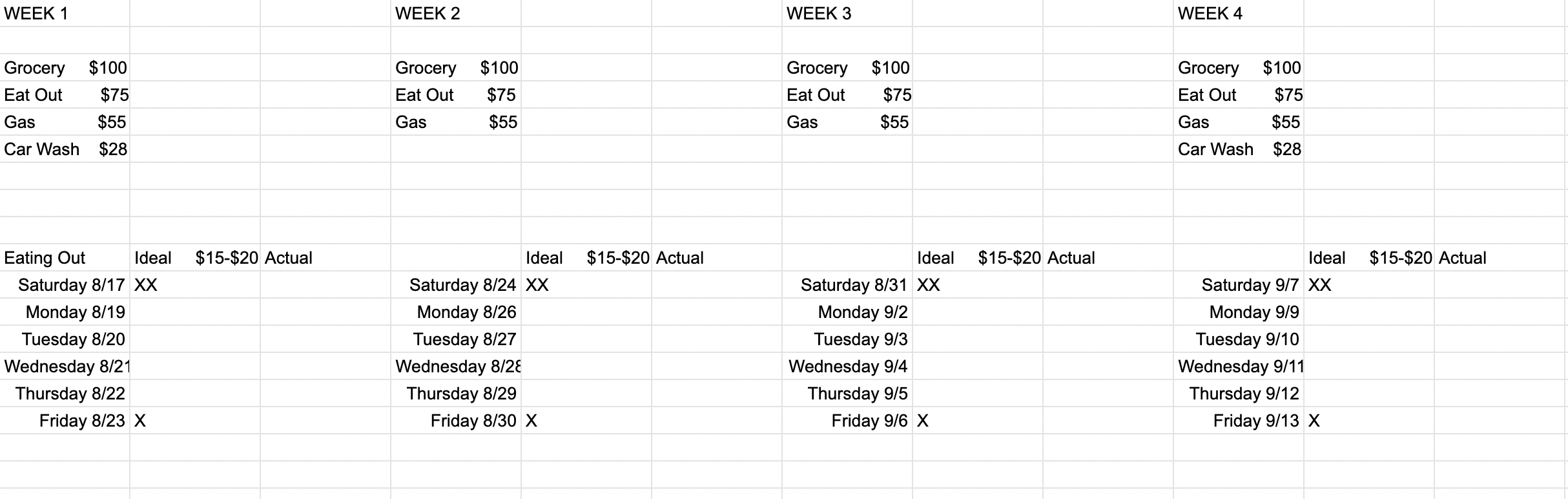

After setting up a budgeting schedule, I like to list how much I earn during this time increment, what fixed payments I have to make (think: car payments, rent, mortgage), and how much I plan to save each month. Once I have those calculated, I will see how much I have left to spend each month by subtracting those payments and the amount I plan to save by the income. See example below. In this model I am using a 4 week budget increment and I am using easy sample numbers.

Next I set aside a budget for monthly items such as Utilities, Subscription Services, Medicine, Clothes, Home Supplies, Beauty Expenses, among other things. I also create a Total Expenses column to generate the amount I will spend each month on things like Groceries, Eating Out, Car Wash, etc. This is where you can evaluate what is important to you.

*Note: Make sure to refer to what you actually spend a month on. What makes an unrealistic budget is not factoring the reality of your expenditures. If you spend $600 a month on eating out, that’s fine! Just figure out where else you can cut back to make it fit within your budget. However, if $600 a month is too much based on your budget then you’re simply going to have to cut back a little bit. Make sure whatever goals you set are realistic and something you can achieve time and time again.

To create my weekly budget, I divide the total expenses by 4 weeks (for the 4 week model option) and see how much I am able to spend each week. I also include a weekly schedule on days I eat out. This might be a little extra, but it keeps me on track to my Eating Out goals. Ideally I only eat out on the weekends, but again if you have different goals, make sure to include them here.

Tip #4: Factor In Yearly Expenditures

My last tip is to factor in your yearly expenditures. This is something that I didn’t do the best at in 2021. When I evaluated my budget, I realized I overspent not on my monthly budget but it’s because I didn’t take the time to plan out my yearly or multi-annual expenditures. These are things like paying your taxes, car registrations, annual subscriptions, birthday gifts, travel, basically all the above. I went way over simply because I didn’t make a plan. Make sure you create a budget that aligns with your lifestyle and keep track of how much is going in and out of your accounts on a yearly basis because over time they really add up.

I hope this has given you some insight on how to create a budget. As always, I have given you enough information for you to create your own budgeting template. However for those wanting to download an already automated budgeting template, I have made my budgeting templates readily available for you. This Budgeting Bundle goes deeper into the financial habits that have helped me achieve my money goals and create a solid financial foundation for myself.